In high-performing dealerships, F&I approval decisions happen in under 60 minutes for prime credit deals — while delays beyond 2 hours dramatically increase deal fallout. Documentation automation alone can reduce paperwork time from 35 minutes to under 10 per deal, unlocking more daily capacity without adding staff.

This guide reveals 5 strategies that transform scattered processes into revenue-generating workflows. You’ll learn how to connect sales and F&I operations, create real-time visibility across all deal stages, automate documentation, and track the metrics that drive consistent profitability.

Try monday CRMKey takeaways

- Track every stage from initial contact through funded contract to spot bottlenecks before they cost you revenue.

- Use connected pipelines to automatically transfer complete deal information between departments, preventing the communication gaps that stall deals.

- Create dashboards that show current deal status, lender responses, and pending stipulations instantly so managers can intervene before approvals expire.

- Reduce paperwork time from 35 minutes to 8 minutes per deal by automating document preparation and stipulation tracking.

- Monitor time from credit application to approval, F&I product penetration rates, and deals lost between departments to identify your biggest revenue opportunities.

- Connect your entire workflow from lead to funded deal with a unified platform that eliminates information silos and automates handoffs between teams.

What is auto sales and finance operations management?

Auto sales and finance operations management covers everything from the moment a customer walks onto the lot to the moment their loan gets funded. This means managing sales workflows, finance and insurance (F&I) functions, regulatory compliance, and the critical handoffs between departments that determine whether deals close smoothly or fall apart.

The difference between selling cars and managing operations? It shows up in your bottom line. When operations run smoothly, customers leave satisfied, deals fund fast, and revenue becomes predictable. When they don’t, deals stall in F&I for days, stipulations get missed, and revenue disappears.

Think about what happens after a customer agrees to buy. That commitment kicks off a complex sequence:

- Credit applications

- Lender communications

- Product presentations

- Documentation

- Funding coordination

Each step requires specific expertise and timing. The dealerships that master this operational flow consistently hit their targets. Those that don’t struggle with unpredictable revenue and frustrated customers.

Understanding auto sales and finance operations fundamentals

Before implementing efficiency strategies, you need to understand the operational framework that drives dealership success. These fundamentals establish the foundation for everything that follows — from terminology to deal flow to departmental functions.

Master key terminology in dealership operations

Shared terminology enables faster handoffs and clearer accountability across sales and F&I teams. Here are the core terms you need to know:

- F&I (Finance and Insurance) is the department that arranges financing, presents protection products like warranties and GAP coverage, and ensures documentation meets regulatory requirements

- Deal flow refers to how transactions progress from initial contact through funded contract, determining whether deals move efficiently or stall

- Funding is when the lender releases payment to the dealership—the true completion point of any sale

- Deal jacket refers to the complete collection of documents needed for a vehicle sale, including credit applications, purchase agreements, and compliance disclosures

Map the complete deal flow from test drive to funded contract

Every customer journey through your dealership involves 8 distinct operational stages. Know who owns each stage and where deals typically fail. That’s how you spot bottlenecks before they cost you revenue.

| Stage | Primary owner | Key activities | Common failure points |

|---|---|---|---|

| Initial contact | Sales | Capture lead info, schedule appointments, build profiles | Incomplete data, poor follow-up |

| Vehicle selection | Sales | Match customer to vehicle, discuss pricing, gather financial info | Unrealistic expectations, overlooked qualification |

| Sales-to-F&I handoff | Sales → F&I | Transfer customer info, terms, vehicle details | Information loss, timing delays |

| Credit application | F&I | Collect financial data, submit to lenders | Incomplete apps, wrong lender selection |

| Lender decision | F&I | Track responses, structure optimal terms | Slow tracking, missed approvals |

| Product presentation | F&I | Present financing and protection products | Rushed presentations, poor matching |

| Documentation | F&I | Complete contracts and required paperwork | Missing signatures, compliance errors |

| Funding and delivery | F&I + Delivery | Submit documents, receive funding, deliver vehicle | Incomplete stipulations, funding delays |

Understand core functions of F&I departments

F&I departments operate under constant pressure. Customers wait, sales teams need deals completed, and lenders have strict deadlines. Understanding these 4 core functions explains why F&I efficiency directly impacts dealership success:

- Financing arrangement requires evaluating credit profiles, maintaining lender relationships, and knowing each lender’s approval criteria. With current new-car loan rates averaging 7.22% at commercial banks, skilled F&I managers know which lenders approve specific profiles, what documentation each requires, and how to structure deals for maximum approval likelihood.

- Product presentation and sales involves matching protection products to customer needs. Extended service contracts, GAP coverage, and prepaid maintenance generate significant revenue while providing genuine customer value when properly presented.

- Compliance management means navigating Truth in Lending Act disclosures, Equal Credit Opportunity Act requirements, and dozens of other regulations. Compliance failures result in substantial fines and legal liability that can devastate a dealership — recent enforcement actions have resulted in penalties exceeding $120,000 for violations involving illegal repossessions and inadequate compliance controls.

- Documentation and funding encompasses preparing accurate contracts, collecting signatures, and ensuring timely funding.

Identify why traditional processes create bottlenecks

Three bottlenecks plague dealerships using outdated methods, each creating problems that multiply across the operation.

- Information fragmentation happens when customer data lives in the CRM, vehicle details sit in the DMS, and F&I documents exist only on paper. Staff manually re-enter the same information multiple times, introducing errors and wasting hours daily.

- Manual status tracking forces managers to physically check with staff or shuffle through paper deal jackets to answer basic questions. When leadership asks about pending deals or stipulation status, nobody has immediate answers.

- Sequential processing limitations mean F&I can’t begin until sales completes their portion entirely. A deal that could finish in 2 hours with parallel processing stretches to 5 hours or more, frustrating customers and limiting daily capacity.

These fundamentals are well understood across the industry. What separates top-performing dealerships is execution. The strategies later in this article focus on redesigning workflows so information moves automatically, decisions happen faster, and deals stop stalling between departments.

Common auto sales and finance workflow challenges

Even experienced dealerships with talented staff hit the same operational challenges. The problem isn’t performance — it’s process design. These problems need more efficient systems, not just harder work from your team. Here are the top workflow challenges costing dealerships revenue every single day.

Challenge: Fragmented communication between sales and F&I teams

Sales and F&I teams naturally develop different priorities. Sales focuses on getting commitments. F&I focuses on structuring sound deals. With the right systems, these different priorities align to create seamless communication that secures deals.

Here’s what derails deals daily:

- Incomplete financial information: Sales provides rough estimates to F&I, forcing them to re-collect data from customers who thought they were finished with questions.

- Hidden credit issues: F&I discovers problems sales missed during qualification, requiring renegotiation after emotional commitment.

- Impossible promises: Sales commits to payment amounts F&I cannot deliver based on actual approval terms.

Picture this: A sales rep shows $35,000 vehicles to a customer with a 580 credit score. Hours later, F&I discovers this customer only qualifies for $22,000 financing. The customer feels deceived, trust evaporates, and the deal often dies completely.

Challenge: Manual tracking of multi-stage approval processes

Most dealerships work with 15 to 25 lenders simultaneously. Each has different criteria, requirements, and response times. A single deal might go to 5 lenders to find optimal terms.

Manual tracking creates chaos. F&I managers maintain spreadsheets listing which applications went where. Staff check multiple lender portals individually for decisions. Stipulations get tracked on paper or in memory. No alerts exist when lenders respond or deadlines approach.

The consequences pile up fast:

- Missed opportunities: Approvals expire because nobody saw the lender’s response in time.

- Lost deals: Stipulations aren’t completed before deadlines pass.

- Wasted time: Staff spend hours daily checking portals instead of closing deals.

Challenge: Lost deals during financing handoffs

The transition from sales to F&I represents the highest-risk moment in any deal. The customer has emotionally committed but hasn’t signed paperwork. They sit waiting, often for 30 to 90 minutes, while F&I prepares documents. That wait time breeds buyer’s remorse.

Handoff failures happen in these ways:

- Information loss: Critical details sales gathered never reach F&I.

- Timing delays: F&I is busy with another customer, extending wait times.

- Expectation mismatches: Sales indicated approval but F&I finds different terms.

5 strategies for improving auto sales and finance efficiency

These strategies here fix operational challenges through better process design and information flow — not by asking staff to work harder. Each strategy builds on the others to transform operations and drive real results.

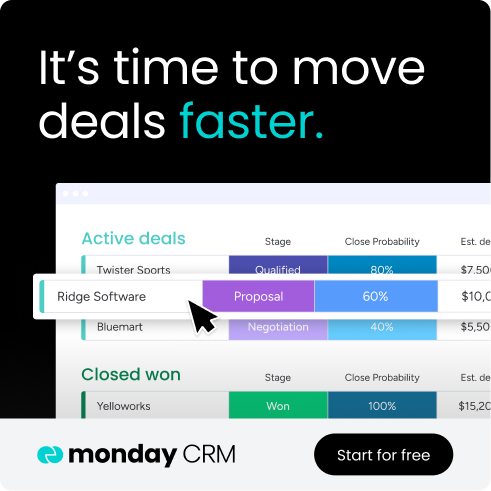

1. Build connected workflows from lead to delivery

Connected workflows create a single system where information flows automatically from initial contact through final delivery. Each department accesses and updates the same record instead of maintaining separate silos.

Here’s what changes immediately:

- Single source of truth: Sales captures information once, and it’s instantly available to F&I and management.

- Automatic progression: Deals advance through stages with automatic status updates and team notifications.

- Complete context: F&I sees which vehicles customers considered, what objections they raised, and what payment ranges they discussed.

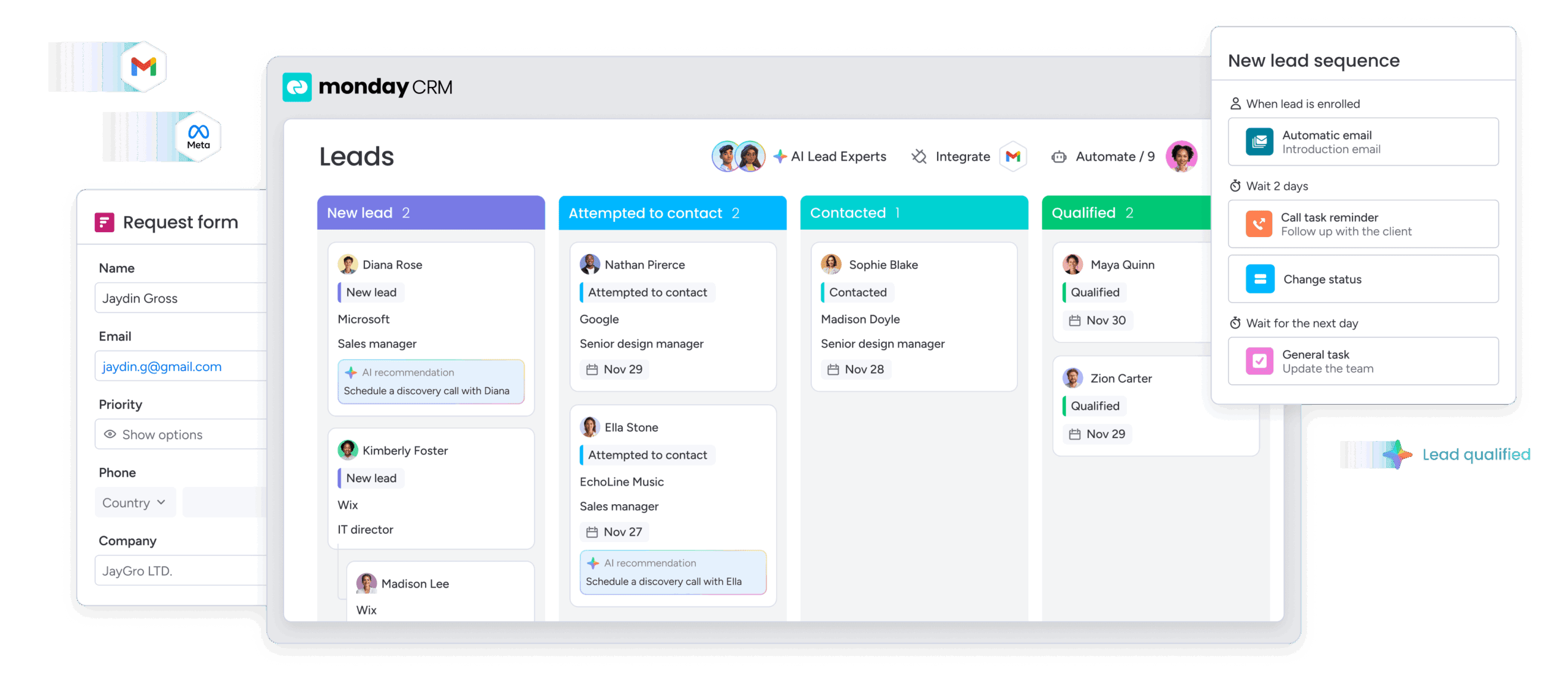

Organizations achieve this connected approach with monday CRM by configuring deal pipelines that match their exact process. Teams set up automatic alerts when deals move between stages, ensuring F&I knows what’s coming before sales physically hands anything off.

2. Create real-time visibility across all deal stages

Real-time visibility means you see deal status instantly, spot bottlenecks as they happen, and access performance metrics on demand. Different roles need different views to make smart decisions.

F&I managers need visibility into incoming deals, lender status, stipulations, and funding deadlines.- Sales managers need visibility into the F&I queue, stage timing, and rep performance.

- General managers need visibility into the total pipeline, bottlenecks, and revenue metrics.

AI-powered visibility goes beyond static dashboards. Instead of managers hunting for problems, AI highlights aging deals, flags approval-risk scenarios based on historical fallout, and predicts which stipulations are most likely to delay funding. Rather than reacting to stalled deals, teams intervene while there’s still time to save them.

This visibility lets managers act before problems escalate. When 6 deals wait for F&I but only 2 sit in sales, managers can reallocate resources immediately. When a deal sits in “pending stipulations” for 3 days, intervention happens before the approval expires.

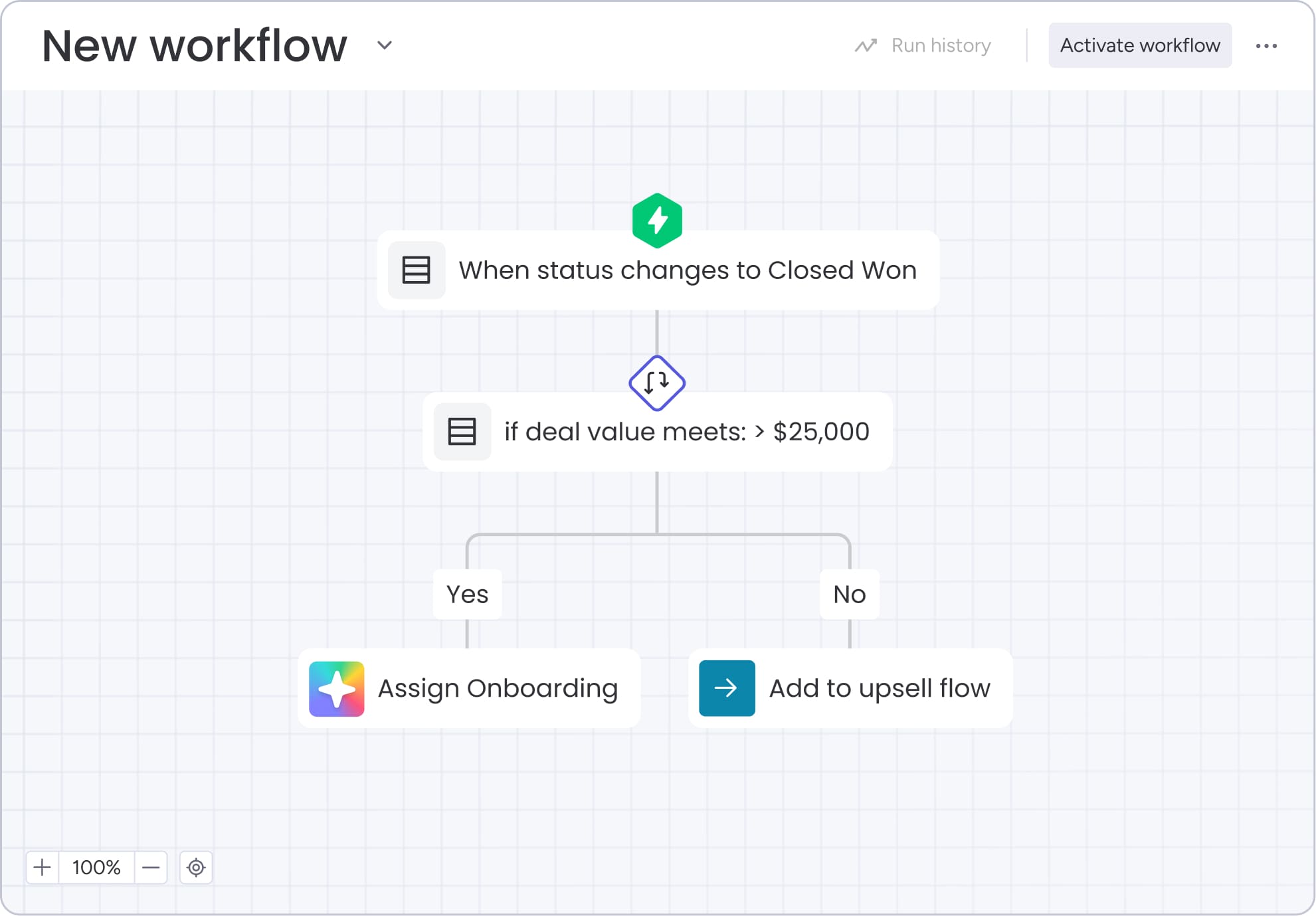

3. Automate repetitive F&I documentation tasks

F&I managers typically spend 40 to 50 percent of their time on paperwork rather than customer interactions. Each deal requires 15 to 25 documents, from credit applications to compliance disclosures.

Here’s what automation changes:

| Task | Manual process | Automated process | Time saved |

|---|---|---|---|

| Document prep | 25–35 minutes | 5–8 minutes | 20–27 minutes |

| Stipulation tracking | 10–15 minutes daily | 2–3 minutes daily | 8–12 minutes |

| Lender formatting | 5–10 minutes per lender | Automatic | 5–10 minutes |

Triggers matter here: Document generation should begin the moment lender approval is received, not when an F&I manager manually starts paperwork. Automated stipulation tasks should trigger the same day approvals arrive — with deadlines tied directly to lender expiration dates.

With monday CRM’s AI capabilities, you can enhance automation further by extracting information from uploaded documents and auto-populating forms. When stipulations arise, the platform creates specific tasks with deadlines and sends automatic reminders as due dates approach.

4. Streamline multi-lender decision making

Successful dealerships work with multiple lenders, each serving different customer segments. Managing these relationships efficiently means submitting to multiple lenders at once and matching customers to the right ones.

Here are the 3 components of streamlined multi-lender workflows:

- Parallel submissions: Send applications to multiple appropriate lenders simultaneously.

- Intelligent matching: Route applications based on customer credit profiles.

- Automated comparison: Evaluate multiple approvals to identify optimal terms.

Here’s how it works: A customer with a 640 credit score applies for financing. The F&I manager enters application details once. The system submits to 5 pre-selected lenders simultaneously. Within 30 minutes, 3 responses arrive with different terms. The platform calculates which option offers the best combination of rate, terms, and dealer participation.

AI-assisted lender matching accelerates this process further by learning from historical approvals. Based on credit profile, deal structure, and prior lender behavior, AI recommends which lenders are most likely to approve — reducing unnecessary submissions and shortening approval cycles without limiting options.

5. Track every special finance deal systematically

Special finance deals need more attention than prime credit transactions. They involve more lender submissions, more stipulations, and take longer to complete. The “$1500 down payment car deal” represents this challenging but profitable segment.

Track special finance deals with:

- Stipulation management: Track exact requirements for each lender with automated deadline alerts.

- Response monitoring: Know immediately when lenders respond or when follow-up is overdue.

- Communication logging: Maintain complete records when multiple staff members work the same deal.

Teams using monday CRM create dedicated pipelines for special finance with appropriate stages, automated reminders, and communication templates that ensure nothing falls through the cracks.

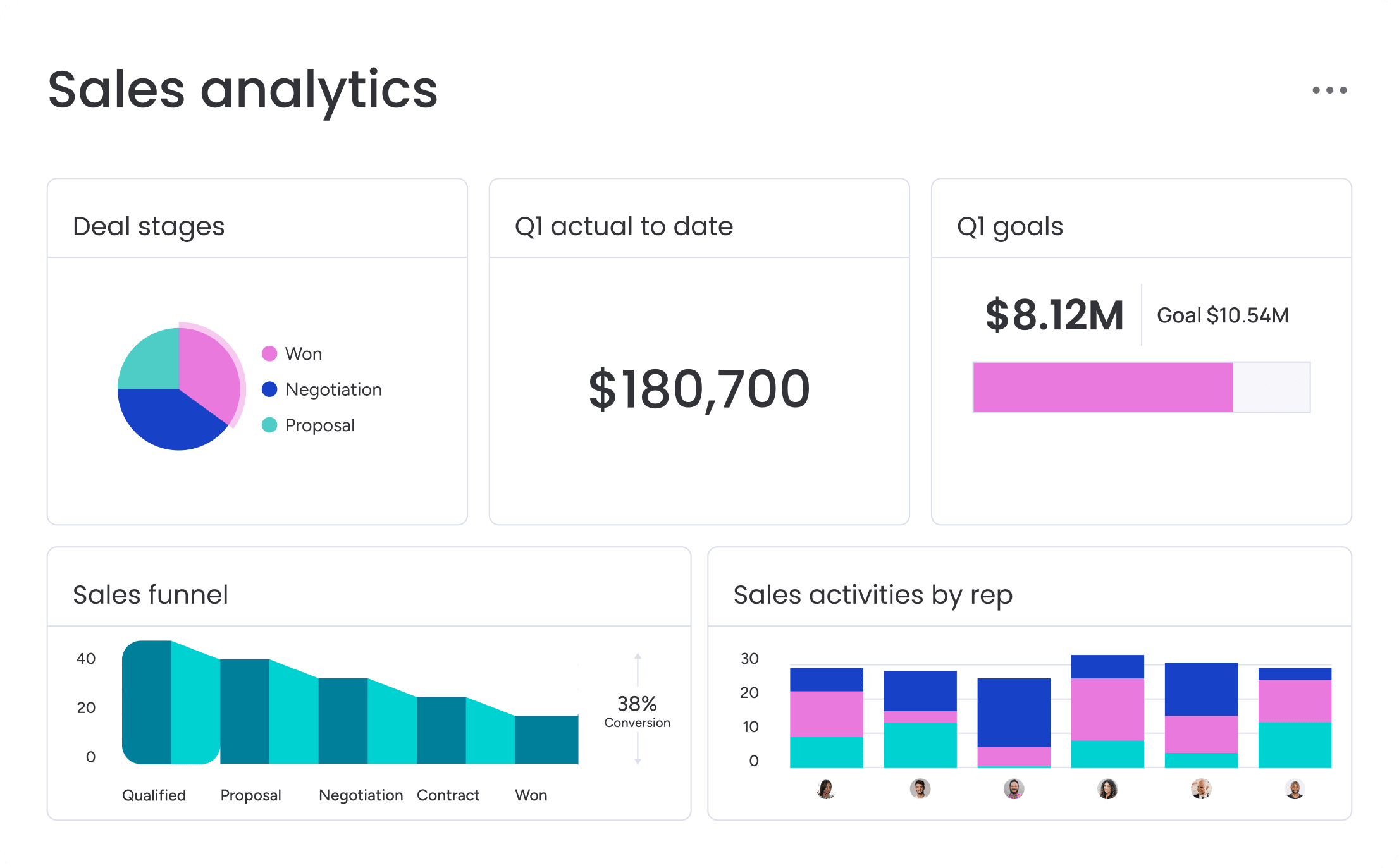

Essential metrics for auto finance operations

Static reports show what already happened. AI-driven trend detection shows what’s about to happen. By analyzing timing patterns, fallout rates, and stipulation delays, AI surfaces emerging risks early — before they appear in month-end reports.

Time from credit application to approval

This metric reveals how efficiently your F&I team processes applications and manages lender relationships. Faster approvals mean happier customers and more daily deals.

| Credit type | Excellent timing | Acceptable timing | Problem indicator |

|---|---|---|---|

| Prime credit | 30–60 minutes | 60–90 minutes | Over 2 hours |

| Special finance | 2–4 hours | 24–48 hours | Over 3 days |

AI monitoring can flag deals likely to exceed acceptable timing thresholds, prompting proactive intervention before customers disengage.

F&I product penetration rates

Product penetration measures the percentage of deals where customers purchase F&I products. A dealership completing 100 deals monthly with 60 percent penetration earns significant product revenue. Increasing penetration to 75 percent adds substantial monthly income without needing more customers.

Deals lost between departments

This metric tracks deals that fall apart during handoffs. Many dealerships never formally track this, missing massive revenue losses.

| Loss cause | Typical frequency | Prevention strategy |

|---|---|---|

| Excessive wait time | 30–40% of losses | Real-time availability visibility |

| Approval term mismatch | 25–35% of losses | Improved communication protocols |

| Customer reconsideration | 15–25% of losses | Faster handoff processes |

Transform auto sales and finance operations with monday CRM

The dealerships winning in automotive retail aren’t just selling cars — they’re running tight operations that maximize every opportunity. Smart operational design turns scattered processes into revenue-generating machines that work predictably.

With monday CRM, you can connect your entire dealership workflow from lead to funded deal, serving as your operational command center that links sales and F&I without replacing your DMS. Here’s what changes when you implement it:

- Unified deal tracking: See every deal from initial contact through funded contract in one place, eliminating information silos between sales and F&I.

- Automated handoffs: Transfer complete customer information, vehicle details, and sales notes automatically when deals move to F&I, preventing the communication gaps that kill deals.

- Real-time lender management: Track submissions to multiple lenders simultaneously, receive instant notifications when approvals arrive, and compare terms side-by-side.

- Smart stipulation tracking: Create automatic tasks for each stipulation requirement with deadline reminders that ensure nothing expires.

- Custom dashboards: Build role-specific views showing exactly what each team member needs — incoming deals for F&I managers, pipeline metrics for general managers, performance data for sales leaders.

- Document automation: Generate contracts and compliance forms automatically using deal information already in the system, reducing paperwork time from 35 minutes to 8 minutes per deal.

Real-time dashboards create predictable revenue with custom views showing deals by stage, days in pipeline, and pending stipulations. Leaders move from high-level metrics to individual deal details instantly, spotting bottlenecks before they hurt revenue. Forecasting views project monthly performance based on current pipeline, replacing end-of-month surprises with predictable results.

Plus, monday CRM adapts to your process because every dealership runs differently. Build custom pipelines for your sales process, F&I workflow, and special finance deals. Create fields for the data points that matter to your dealership. Change workflows instantly as your process evolves — no IT help needed.

Start building your revenue-generating operations machine

Connected workflows, real-time visibility, documentation automation, streamlined multi-lender decisions, and systematic special finance tracking transform chaotic handoffs into smooth operations that close more deals faster. When information flows automatically between departments, when managers spot bottlenecks before they cost revenue, and when documentation takes minutes instead of hours, your dealership stops losing deals to operational friction.

Ready to turn scattered processes into predictable revenue? Try monday CRM free and see how connected workflows eliminate the gaps between sales and F&I that are costing you deals every single day. Build your first pipeline in minutes, automate your handoffs, and start tracking the metrics that matter — no credit card required.

Try monday CRMFAQs

What is the difference between F&I and sales in a dealership?

The difference between F&I and sales lies in their functions: sales departments help customers select vehicles and negotiate prices, while F&I departments arrange financing, present protection products, ensure compliance, and complete documentation after purchase agreement.

How long should the F&I process take?

The F&I process should take 45 to 90 minutes for most transactions, with prime credit customers completing in 45 to 60 minutes and special finance customers requiring 2 to 4 hours initially plus additional documentation time.

What are the most common reasons deals fall through in F&I?

The most common reasons deals fall through include credit approval issues, excessive wait times causing reconsideration, missing documentation requiring return visits, and payment terms exceeding customer comfort levels.

How many lenders should a dealership work with?

A dealership should work with 15 to 25 lenders to serve the full credit spectrum, including prime lenders, captive finance companies, non-prime lenders, and special finance specialists.

What technology do F&I departments need?

F&I departments need deal tracking and pipeline management, lender integration for submissions, document generation and management systems, compliance tools, and comprehensive communication tracking capabilities.

How can dealerships improve special finance deal completion rates?

Dealerships improve special finance completion rates through systematic stipulation tracking, proactive customer communication before deadlines, multiple simultaneous lender submissions, realistic expectation setting, and dedicated workflows for complex deals.