Household debt reached $18.8 trillion at the end of 2025, with mortgage balances alone topping $13 trillion. Behind every one of those loans sits an amortization schedule, the payment-by-payment roadmap that breaks a lump sum into manageable monthly installments. An amortization schedule Excel template turns that roadmap into something you can actually build, adjust, and track without starting from scratch.

Whether you’re managing a 30-year mortgage, an auto loan, or a student loan refinance, a solid template does the heavy lifting. It preloads the formulas, organizes principal and interest splits, and lets you model “what if” scenarios, such as extra payments or rate changes, in seconds.

In this guide, you’ll learn what amortization schedules are, how to create one in Excel step by step, how extra payments can save you thousands, and how platforms like monday AI Work Platform can take your loan tracking beyond a single spreadsheet.

Get started with monday.comKey takeaways

- An amortization schedule Excel template pre-loads PMT, IPMT, and PPMT formulas so you can map every payment from the first installment to the final payoff without building calculations from scratch

- Early loan payments go mostly toward interest; understanding this split helps you decide when and how extra payments make the biggest impact

- Even $200 per month in additional principal on a $250,000 mortgage can cut roughly seven years off the term and save over $100,000 in interest

- Fixed-rate and adjustable-rate loans require different template structures, so matching the right template to your loan type is essential for accurate tracking

- monday AI Work Platform lets you import Excel amortization schedules into a collaborative workspace with automations, dashboards, and real-time visibility across multiple loans

What is an amortization schedule Excel template?

An Excel amortization schedule template is a pre-structured document with fillable fields that helps you fill out a loan amortization schedule. A template simplifies what can often be a complex process with many difficult formulas.

Amortization involves breaking a fixed-rate loan into equal monthly payments to pay off by a certain date. It’s used commonly for mortgages, auto loans, student loans, and personal loans. Amortization allocates principal and interest to each payment, ensuring you pay both, and provides predictable payments for the borrower.

When amortizing a loan, your first loan payment consists mostly of interest. As you reduce the principal balance, less interest is charged per payment. Thus, each successive payment consists of more principal than the last.

A finished Excel amortization schedule lays out monthly payments and shows how much of each payment is principal vs. interest. This is where a template comes in.

How amortization math works

The mechanics are straightforward once you see the pattern. Every monthly payment is the same dollar amount, but the split between principal and interest shifts over time. Early in the loan term, most of your payment goes toward interest because the outstanding balance is large. As the balance shrinks, the interest portion decreases while the principal portion increases.

For example, on a $250,000 mortgage at 6.5% over 30 years, your monthly payment is about $1,580. In month one, roughly $1,354 goes to interest, and only $226 goes to principal. By month 300, those numbers nearly flip. A loan amortization schedule Excel template captures this entire progression automatically, so you don’t have to calculate each period by hand.

It’s worth noting that amortization applies specifically to loans: the gradual repayment of debt. Depreciation, by contrast, spreads the cost of a physical asset (like equipment or a vehicle) over its useful life. Both involve spreading costs over time, but they apply to different financial contexts.

Get started with monday.comWhy use an amortization schedule Excel template?

Loan amortization schedules help you turn a long-term loan into a predictable monthly payment. As a result, you can budget for that monthly payment more easily and reduce the risk of default.

But this isn’t something you can calculate in your head. Luckily, amortizing a loan is much easier with an amortization schedule Excel template. Here are some reasons to use this type of template:

Save time on creating new schedules

You can simply save your Excel template as a new file each time to quickly create new amortization schedules. This will save you a lot of time designing, building, and adding formulas to your amortization schedules.

Avoid miscalculations with accurate pre-created formulas

Excel amortization templates include prewritten formulas in cells to automatically calculate the data you need.

In a good amortization Excel template, you only need to enter a few numbers, and formulas will take over and fill out the entire table for you. No need to change each individual box if you make an error, simply fix the input number, and the formulas will adjust.

Cloud-based if using Microsoft 365

Microsoft 365 allows you to take your Excel spreadsheet to the cloud. That way, you can access your amortization table from anywhere you have a device and an internet connection.

Model different payment scenarios

A simple loan amortization schedule in Excel lets you test different outcomes instantly. Want to see how a $200 extra monthly payment affects your payoff date? Change one cell. Curious how refinancing at a lower rate would reduce total interest? Swap the rate and compare. Templates make scenario modeling accessible without any spreadsheet expertise.

Create an audit trail for your loans

Each saved version of your amortization schedule becomes a snapshot of your loan at a specific point in time. If you refinance, make lump-sum payments, or renegotiate terms, you’ll have a documented history showing exactly how your payment structure evolved. That record is invaluable during tax season or when applying for new credit.

Examples of amortization schedule Excel templates

Now that we’ve covered the benefits, let’s dive into the nitty-gritty and explore some actual templates.

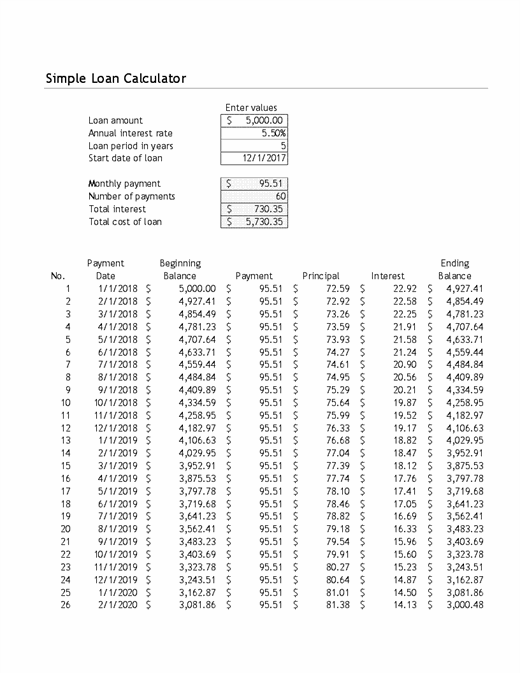

Microsoft’s Excel loan amortization schedule

This is Microsoft’s official basic amortization schedule template for Excel. As you can see, it has a few fields to enter loan information, such as the loan amount and interest rate.

Then it includes an amortization table detailing each monthly payment. It also helps you see how many of your dollars go toward principal vs. interest. This template does the job, but adding some color and other design elements could make it easier to read and understand.

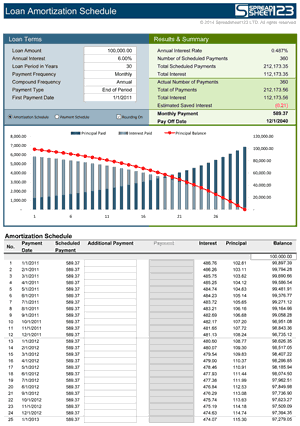

Amortization schedule Excel template with chart

Here, we have an Excel amortization template with several design elements that provide additional visual information.

In particular, the chart shows you how each successive payment covers more principal as the total loan balance decreases. Plus, there’s a line for “estimated saved interest,” which can tell you how much total interest you’d save by paying more than the minimum payment. This template also uses colors to create visual appeal and draw your eye to specific information.

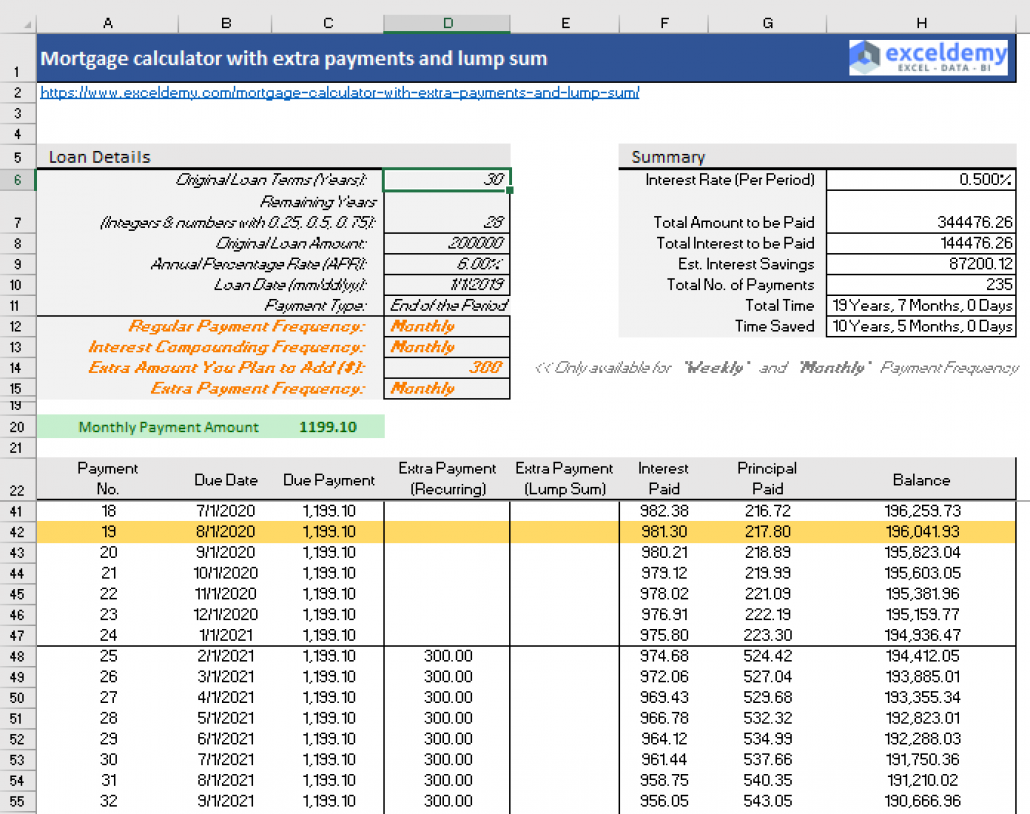

Mortgage amortization schedule template with extra payments

This Excel template contains a typical loan amortization schedule, with boxes at the top for loan info and a table that lays out each monthly payment.

However, it also includes a few boxes where you can add information about extra payments, both the amount and the frequency. You can choose between weekly and monthly frequency.

As a result, you can project how much faster you’d pay off a loan given a certain payment amount and how much you could save on interest.

How to create an amortization schedule in Excel

You don’t need a pre-built template to get started. With three core Excel formulas, you can build a fully functional amortization schedule from scratch. Here’s how to create one step by step.

Step 1: Set up your loan parameters

Start by entering your loan details in a dedicated section at the top of your spreadsheet. You’ll need four values:

- Loan amount: The total principal borrowed (e.g., $250,000)

- Annual interest rate: The yearly rate from your lender (e.g., 6.5%)

- Loan term in years: The repayment period (e.g., 30 years)

- Start date: When your first payment is due

Place these in cells you can reference throughout the sheet. Something like B1 through B4 works well. Lock them with dollar signs ($B$1) so your formulas stay accurate when you drag them down.

Step 2: Calculate your monthly payment with PMT

The PMT function calculates your fixed monthly payment amount. The syntax is:

=PMT(rate/12, term*12, -loan_amount)

For our example: =PMT(6.5%/12, 30*12, -250000) returns approximately $1,580.17 per month. The negative sign on the loan amount tells Excel this is money you owe, and the result comes back as a positive number representing your payment.

One common mistake to avoid: always divide the annual rate by 12 for monthly payments. Using the annual rate directly will produce wildly incorrect results.

Step 3: Calculate interest per period with IPMT

The IPMT function tells you exactly how much of each payment goes toward interest. The syntax is:

=IPMT(rate/12, period, term*12, -loan_amount)

The “period” argument changes row by row: period 1 for month 1, period 2 for month 2, and so on. For month one of our example: =IPMT(6.5%/12, 1, 360, -250000) returns about $1,354.17.

Step 4: Calculate principal per period with PPMT

The PPMT function handles the principal portion. The syntax mirrors IPMT:

=PPMT(rate/12, period, term*12, -loan_amount)

For month one: =PPMT(6.5%/12, 1, 360, -250000) returns about $226.00. Notice that PMT = IPMT + PPMT for every single period. That’s the fundamental check that confirms your schedule is accurate.

Step 5: Build the schedule table

Create columns for each of these values, plus a running balance:

- Column A: Payment number (1, 2, 3…)

- Column B: Payment date

- Column C: Monthly payment (PMT)

- Column D: Principal portion (PPMT)

- Column E: Interest portion (IPMT)

- Column F: Remaining balance (previous balance minus principal)

Fill in row one with your formulas, then drag them down for the full loan term (360 rows for a 30-year mortgage). The remaining balance in your final row should be $0.00 (or very close to it, accounting for rounding).

Step 6: Verify your totals

Use SUM formulas at the bottom of your columns to confirm accuracy. The sum of all principal payments should equal your original loan amount. The sum of all payments minus the sum of all principal gives you the total interest paid over the life of the loan. For our $250,000 example at 6.5%, you’d pay roughly $318,861 in total interest over 30 years.

Get started with monday.comHow extra payments change your amortization schedule

One of the most powerful features of an amortization schedule is its ability to model the impact of extra payments. Even modest additional principal payments can dramatically reduce your total interest and shorten your loan term.

To add extra payments to your Excel template, insert a new column next to your standard payment column. In your balance formula, subtract both the regular principal portion and the extra payment from the previous balance. The formula looks something like this:

=Previous_Balance - PPMT_Amount - Extra_Payment

On that same $250,000 mortgage at 6.5% over 30 years, adding just $200 per month in extra principal payments would:

- Cut roughly 7 years off your loan term

- Save approximately $108,000 in total interest

- Pay off the loan in about 23 years instead of 30

Your amortization schedule with fixed monthly payment columns makes this comparison visual and immediate. You can see exactly which month your loan hits zero under each scenario and decide whether the extra payment fits your budget.

Fixed-rate vs. adjustable-rate amortization: what changes

Not every loan follows the same amortization pattern. Understanding the difference between fixed-rate and adjustable-rate loans helps you choose the right template and set realistic expectations.

Fixed-rate loans are the simpler case. Your interest rate stays the same for the entire term, which means your monthly payment never changes. The amortization schedule is fully predictable from day one, and every row is calculated at the same rate. Most standard Excel amortization templates assume a fixed rate.

Adjustable-rate mortgages (ARMs) introduce a variable. After an initial fixed period (commonly five or seven years), the rate resets periodically based on a market index. When the rate adjusts, your monthly payment changes, and the principal-interest split recalculates. As of June 2026, 30-year fixed rates are around 6.52% according to Freddie Mac, while initial ARM rates may start lower and then adjust upward.

If you’re working with an ARM, your Excel template needs additional logic, such as multiple rate inputs for each adjustment period or a lookup table that changes the rate at specified intervals. For most personal finance scenarios, a fixed-rate template is the practical starting point.

Amortization schedule tips to get more from your template

Now that you’re all set with a template, let’s cover a few tips for how to make the most of it.

1. Input formulas

Formulas in Excel, and on monday AI Work Platform, can save you a lot of time doing the math on your amortization schedule. You can create a formula by using the “=” sign and then typing out the formula you want. For instance, if you type “=B1+B2” into B3, Excel will automatically calculate the sum of B1 and B2 and put the result in B3.

Most amortization schedule Excel templates include formulas for the core amortization schedule, but you can modify them as needed or add formulas elsewhere to calculate other relevant information.

2. Use color to highlight data

Excel lets you add colors and format the text to make certain information stand out. This can make it easier to locate that information and distinguish it from other data on the template.

For instance, you can make your payments in the amortization schedule colored red. This indicates that you’re subtracting this amount from your loan balance. It also helps you locate that column more quickly among all the words and numbers within your template.

3. Find templates that suit your examples

Many people have multiple loans of different types, whether for business or personal matters. It’s good to create several amortization schedules to track all your loans, but you may need different templates for each.

For instance, a mortgage amortization schedule with a balloon payment will look different from that of a personal loan with a shorter term and no balloon payment. Your templates should look different to accommodate each type of loan.

Fortunately, you can duplicate Excel templates to create multiple amortization schedules with just a few mouse clicks. Save them with different names, such as “mortgage amortization table,” and you’re good to go.

Track and manage loan amortization with monday AI Work Platform

Excel handles the math well for individual loan schedules. But when you’re juggling multiple loans, coordinating with a partner or financial advisor, or need automated reminders before each payment, a collaborative platform adds capabilities that a static spreadsheet can’t offer.

With monday AI Work Platform, you can import any existing amortization schedule from Excel directly into the platform, preserving your data and structure without manual re-entry.

From there, the platform opens up capabilities that a static spreadsheet can’t match:

From there, the platform opens up capabilities that a static spreadsheet can’t match:

- Formula columns replicate the same PMT, IPMT, and PPMT logic you’d use in Excel, keeping your amortization calculations accurate and up to date

- Automations send payment reminders before each due date, flag overdue payments, and notify team members when a loan milestone is reached, with no manual follow-up required

- Dashboards give you a real-time view across all your loans. See total outstanding debt, upcoming payments, and cumulative interest savings in a single visual workspace

- Real-time collaboration lets you share loan schedules with a spouse, business partner, or financial planning team without emailing spreadsheet versions back and forth

- Custom app builder (monday vibe) lets you describe a custom loan tracking app in plain language and generates a working app from that description. For example, “build me an app that tracks my mortgage, auto loan, and student loan with payment dates and remaining balances” produces a ready-to-use tool in moments

If you already maintain a budget tracker or financial forecast, your amortization schedule fits naturally alongside those workflows. Everything stays connected, visible, and actionable in one workspace.

Get started with monday.comTake control of your amortization schedule

An amortization schedule Excel template transforms what could be a confusing financial obligation into a structured, predictable plan. You know exactly how much you’re paying each month, how the principal-interest split evolves, and how strategies like extra payments can save you significant money over the life of a loan.

Whether you build your schedule from scratch using the PMT, IPMT, and PPMT formulas or start with a prebuilt template, the important thing is to have a system that keeps your loans visible and manageable. For those who need collaboration, automation, and portfolio-level views, monday AI Work Platform extends that amortization schedule Excel template into a connected financial workspace.

Get started with monday.comFAQs

How do I create an amortization schedule in Excel?

An amortization schedule in Excel requires three formulas: PMT for the monthly payment, IPMT for the interest portion, and PPMT for the principal portion. Enter your loan amount, interest rate, and term, apply these formulas across rows for each payment period, and you'll have a complete schedule.

Does Excel have a loan amortization schedule template?

Yes, Excel includes a built-in simple loan amortization schedule template available through the template gallery. It covers the basics, but if you need additional features such as advanced payment modeling or multi-loan tracking, consider a more robust template or a platform like the monday AI Work Platform.

What formulas are used in an amortization schedule?

The three core Excel formulas are PMT (calculates the total monthly payment), IPMT (calculates the interest portion of each payment), and PPMT (calculates the principal portion of each payment). Together, they satisfy the relationship PMT = IPMT + PPMT for every payment period.

How do extra payments affect an amortization schedule?

Extra payments reduce your outstanding principal faster, which lowers the interest charged on subsequent payments. Even small additional monthly payments can shorten your loan term by several years and save tens of thousands of dollars in total interest.

What is the difference between amortization and depreciation?

Amortization spreads loan repayments into scheduled installments over time, while depreciation allocates the cost of a tangible asset (such as machinery or a vehicle) over its useful life. Both distribute costs over time, but amortization applies to debt and depreciation applies to assets.

Can I use Google Sheets for an amortization schedule?

Yes, Google Sheets supports the same PMT, IPMT, and PPMT functions as Excel, so your amortization formulas work identically. For teams that need real-time collaboration, automated reminders, and dashboard views across multiple loans, monday AI Work Platform offers those capabilities alongside standard calculation features.